The Unbundling of Venture Capital

By Jeff Kraft, Managing Partner at Sync.VC

Opening

For most of modern venture capital history, the industry operated on a relatively simple premise:

Investors committed capital to blind-pool funds managed by a small number of venture firms, then waited patiently for distributions over a 10+ year time horizon.

That structure made sense for decades.

Information was fragmented. Access to high-quality private companies was scarce. Private market liquidity was limited. Coordination costs were high. Investors largely depended on institutional firms to source opportunities, construct portfolios, and manage long-duration exposure on their behalf.

In many ways, venture capital evolved around the realities of a far less connected market.

But the assumptions underlying that system are beginning to change.

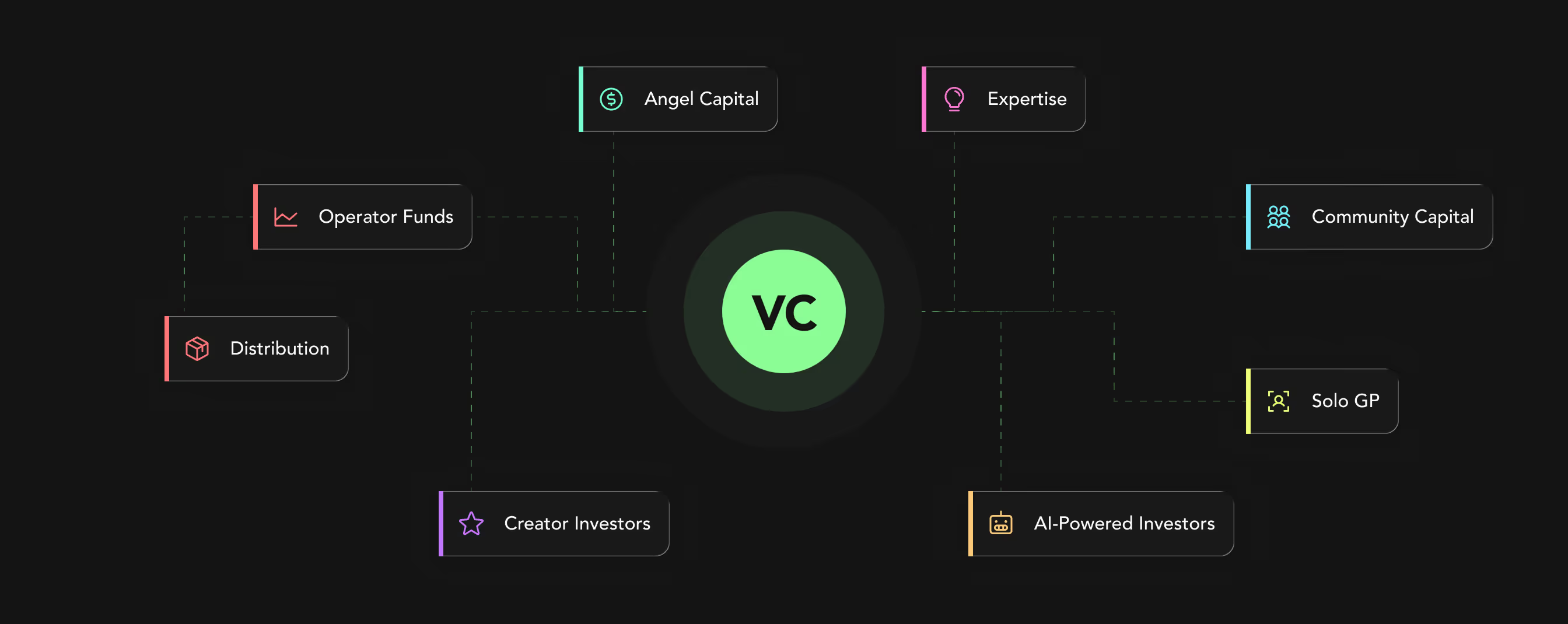

Over the last several years, venture capital has undergone a quiet but profound structural evolution. The rise of solo GPs, SPVs, rolling funds, direct secondaries, and network-driven syndication has fundamentally expanded how capital moves through private markets.

At the same time, venture-backed companies are remaining private dramatically longer than prior generations. Companies that once would have entered public markets after several years now often remain private for a decade or more, accumulating enormous enterprise value entirely within the private ecosystem.

That shift matters.

Historically, venture capital primarily financed company formation.

Increasingly, it finances entire corporate lifecycles.

As a result, investors are demanding more flexibility, more visibility, and more liquidity than the traditional blind-pool structure was originally designed to provide.

The result is not the death of the traditional venture fund.

It is the gradual unbundling of venture capital itself.

From Blind Pools to Precision Exposure

Traditional venture funds were designed around two core realities: access scarcity and diversification.

Limited partners committed capital broadly because they often had limited visibility into the specific companies that would ultimately comprise a portfolio. In exchange, they gained exposure to the sourcing capabilities, network, and judgment of an established manager.

That model still works exceptionally well in many contexts.

But increasingly, sophisticated investors want something different.

They want:

- more concentration,

- more transparency,

- more thematic precision,

- and more direct participation in specific opportunities.

Rather than allocating capital to an entire portfolio in order to gain exposure to a handful of exceptional companies, many investors now prefer selecting individual opportunities directly through SPVs, syndicates, or single-asset vehicles.

In other words, investors no longer necessarily want the whole basket.

They increasingly want the ability to selectively underwrite the assets they believe possess the highest asymmetry.

That is a meaningful shift in investor psychology.

Traditional venture capital largely optimized around manager selection.

Modern venture increasingly optimizes around conviction-driven exposure.

The growth of single-asset structures reflects this broader evolution toward investor-directed portfolio construction.

The Rise of the Solo GP

One of the clearest manifestations of this transition is the continued rise of solo GPs and emerging managers.

Over the last decade, the infrastructure required to launch and operate venture investment vehicles has become dramatically more modular.

Historically, building a venture platform required substantial operational overhead:

- fund administration,

- legal coordination,

- LP management,

- banking,

- compliance,

- SPV formation,

- tax reporting,

- and institutional back-office infrastructure.

Today, much of that stack has become software-enabled.

Platforms like AngelList, Carta, Allocations, and Sydecar have significantly lowered the operational barriers required to launch and manage investment vehicles.

That evolution matters far beyond simple operational efficiency.

It fundamentally changes who can participate as a capital allocator.

As a result, a new generation of highly specialized managers has emerged: operators, domain experts, founders, and deeply networked individuals capable of building highly differentiated investment ecosystems without the institutional scale historically required to do so.

This mirrors broader trends across technology, media, and finance: the decentralization of institutions into networks of specialized individuals.

Just as software unbundled media distribution and enabled the rise of independent creators, venture infrastructure is increasingly unbundling capital formation itself.

Reputation is becoming infrastructure.

Increasingly, investors are backing not simply firms, but individuals with highly specialized access, expertise, and trust networks.

That shift has significant implications for how venture capital is sourced, distributed, and coordinated over the coming decade.

Liquidity Changes Investor Psychology

The rise of venture secondaries may ultimately prove even more important than the rise of SPVs.

Historically, private investments were psychologically treated as locked capital. Investors accepted opacity, illiquidity, and decade-long holding periods because there were few viable alternatives.

That environment is changing rapidly.

As startups remain private longer, secondary markets have expanded dramatically to accommodate growing demand for liquidity from:

- founders,

- employees,

- early investors,

- institutions,

- and late-stage buyers.

Platforms like Forge Global now facilitate billions of dollars in private share transactions while introducing increasingly sophisticated pricing and market data infrastructure around private assets.

This changes far more than liquidity alone.

Secondary markets increasingly function as information systems.

Pricing visibility, transaction activity, and reference liquidity all contribute to a more dynamic and continuously informed private market environment.

Even when investors never actively sell positions, the existence of potential liquidity fundamentally changes how risk is perceived and underwritten.

Liquidity is not merely a transaction mechanism.

It alters investor behavior.

Historically, venture capital behaved almost like a one-way commitment: capital entered and remained structurally trapped until a terminal outcome occurred.

Today, positions can increasingly be:

- partially liquidated,

- strategically increased,

- rebalanced,

- refinanced,

- or transferred.

That changes portfolio construction entirely.

It encourages:

- greater participation,

- more active portfolio management,

- increased concentration,

- and more dynamic ownership strategies across private markets.

In many ways, venture capital is evolving from a terminal asset class into a continuously manageable portfolio asset.

Private Markets Are Becoming Continuous Markets

Historically, venture investing operated through isolated financing events.

Capital entered during discrete funding rounds and exited years later through IPOs or acquisitions.

Today, those boundaries are becoming increasingly blurred.

Investors may:

- participate in a primary financing,

- add exposure later through secondaries,

- selectively increase concentration,

- partially exit positions,

- or dynamically rebalance exposure over time.

This creates something fundamentally different from the historical venture model.

Private markets are beginning to resemble continuously connected market ecosystems rather than isolated capital formation events.

That evolution is accelerating because the infrastructure surrounding private markets continues to mature rapidly.

What once required highly fragmented relationship networks and manual coordination increasingly operates through structured platforms, syndication systems, secondary marketplaces, and software-enabled capital infrastructure.

Importantly, this does not eliminate the role of traditional venture firms.

Large institutional firms will continue to play a critical role in:

- company building,

- recruitment,

- signaling,

- governance,

- and large-scale capital deployment.

But they are no longer the only efficient coordination mechanism within the venture ecosystem.

The market itself is becoming more networked.

Why This Benefits Founders Too

This evolution is not solely beneficial for investors.

Founders increasingly benefit from:

- broader access to specialized capital,

- more aligned investors,

- flexible financing structures,

- and selective liquidity opportunities without requiring full company exits.

Historically, venture ecosystems concentrated power heavily within a relatively small number of institutions.

The emerging model distributes participation far more broadly across networks of operators, specialists, emerging managers, and strategic investors.

That creates a healthier and more dynamic capital environment for many companies.

It also enables founders to build more intentional cap tables composed of investors with differentiated expertise, relationships, and strategic value rather than relying exclusively on generalized institutional capital.

The venture ecosystem is not becoming less institutional.

It is becoming more modular.

The Next Decade of Venture Capital

The most important shift happening in venture capital today is not simply larger funds or larger rounds.

It is flexibility.

The industry is evolving toward:

- modular investment structures,

- network-driven syndication,

- increased pricing transparency,

- investor-directed exposure,

- more dynamic ownership models,

- and increasingly liquid private markets.

Over time, venture capital may begin to resemble less of a static asset class and more of a continuously connected marketplace of capital, relationships, reputation, and conviction.

One where:

- investors can express more precise thematic exposure,

- founders can access more specialized capital,

- and ownership itself becomes increasingly dynamic.

The blind-pool venture fund will remain an important structure.

But it is no longer the only efficient structure.

And increasingly, it may no longer be the default.

Bibliography & Research Sources

- Carta. Small VC Funds Continue to Increase. https://carta.com/data/small-vc-funds-increase-2024/

- IMD. The Rise of Venture Capital Secondaries. https://www.imd.org/ibyimd/finance/the-rise-of-venture-capital-secondaries/

- Forge Global. Private Market Investing & Liquidity Insights. https://forgeglobal.com/

- Reuters. Charles Schwab Strikes Deal for Forge Global. https://www.reuters.com/legal/transactional/charles-schwab-strikes-660-million-deal-private-shares-platform-forge-global-2025-11-06/

- AngelList. Rolling Funds and Syndicate Infrastructure. https://www.angellist.com/

- Allocations. Venture Fund Administration Infrastructure. https://www.allocations.com/

- Sydecar. SPV and Venture Infrastructure Platform. https://www.sydecar.io/

.avif)

.avif)

.avif)